In 2026, regulatory change is a permanent feature of the financial landscape. It shapes daily operations, influences governance decisions, and places continuous demands on systems and people. What was once addressed through scheduled implementation projects now sits at the core of institutional functioning.

The regulatory momentum built during 2024 and 2025 has carried fully into this year. Supervisory expectations continue to intensify. Reporting timelines are tighter. Data quality and consistency are increasingly assessed as signals of institutional preparedness rather than procedural compliance.

For banks, investment firms, payment institutions, and crypto-asset service providers, the pressure in 2026 does not originate from a single regulatory initiative. It stems from the combined effect of overlapping frameworks, parallel reporting streams, and sustained supervisory scrutiny. Regulatory reporting has evolved into an operational discipline with direct implications for credibility and resilience.

In Cyprus, these realities are well understood by Prognosys Solutions. For more than two decades, the company has worked alongside financial institutions as regulatory reporting matured from a technical requirement into a strategic operational capability, supporting more than 80% of the local banking market.

A demanding regulatory cycle

The current regulatory cycle reflects a convergence of European frameworks and supervisory priorities. Central to this is the adoption of the EBA Reporting Framework 4.0, together with the implementation of CRR III and CRD VI. In parallel, investment firms have aligned with the IFR and IFD framework, while MiCAR has brought crypto-asset activities firmly within the regulatory perimeter.

Alongside prudential reform, DORA has reshaped expectations around digital and operational resilience. Reporting obligations now extend deeper into ICT risk, incident management, and third-party dependencies. The direction is consistent. Supervisors expect structured, validated, and coherent data across regulatory domains.

This shift has transformed reporting environments. Institutions are required to deliver high-quality data across prudential, financial, operational, and resilience frameworks, often under compressed timelines and evolving technical standards.

What is already in force

Several regulatory changes became effective at the start of 2026, leaving limited flexibility once reporting deadlines were set.

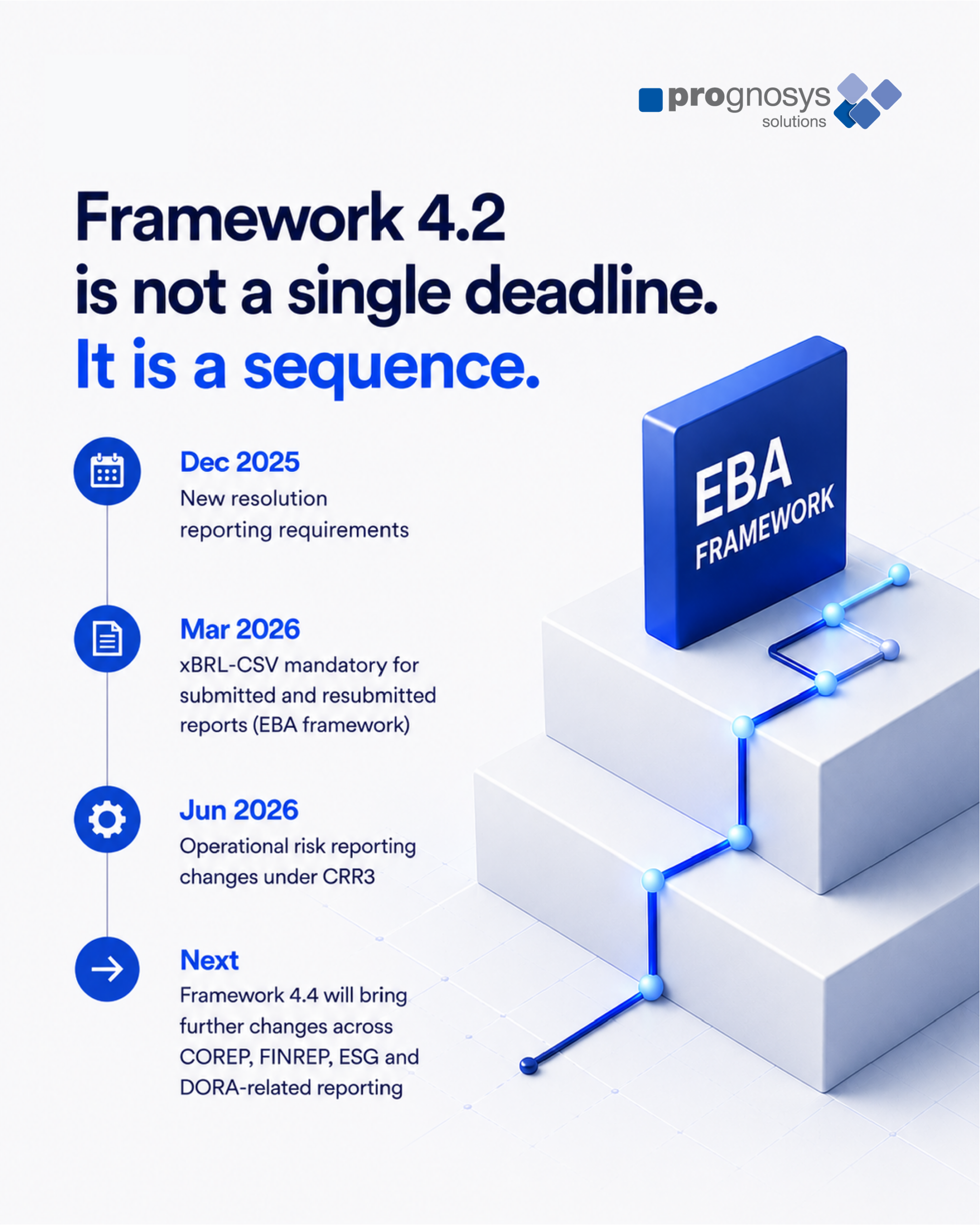

Resolution Planning is a clear example. A revised set of Implementing Technical Standards introduced expanded data requirements and stricter validation rules. Institutions must submit detailed organisational, liability, and critical function information through RESOL 1 and RESOL 2 within the first months of the year, in line with EBA specifications.

At the same time, FINREP for Credit Acquiring Companies became applicable from the 31 December 2025 reference date, following the Central Bank of Cyprus’s introduction of a new reporting template. For affected institutions, this added a new reporting stream with specific data modelling and validation requirements.

Another immediate change is the application of NACE Codes Rev. 2.1 from 1 January 2026. While supervisory guidance has been issued for selected reports, including AnaCredit and CCR, other areas remain subject to interpretation. Reporting teams must therefore apply careful judgement and maintain close oversight as further clarification develops.

The most technically demanding milestone of the year is the mandatory transition of all remaining regulatory reports to XBRL-CSV by 31 March 2026. Linked to the EBA Reporting Framework 4.2, this transition requires changes to report generation processes, validation logic, and testing environments. For many institutions, it represents one of the most resource-intensive reporting initiatives of the year.

An evolving year, not a static one

Regulatory pressure in 2026 does not concentrate in the first quarter. It continues to unfold throughout the year.

Initiatives such as the Pillar 3 Data Hub and DAC 8 reinforce the push towards greater transparency and comparability. Structured reporting now extends beyond supervisory submissions into public disclosures and tax-related reporting for crypto-asset activities.

Instant Payments Reporting introduces harmonised templates and retrospective submission requirements. Payment service providers must revisit historical data while ensuring alignment with current reporting standards.

Additional complexity is expected through expanded operational risk reporting under CRR III and CRD VI, alongside the forthcoming EBA Reporting Framework 4.3. Expected later in the year, Framework 4.3 is anticipated to consolidate changes across FINREP, liquidity, market risk, and selected DORA-related elements.

These developments coincide with the start of direct supervision by AMLA. This marks a new phase in AML oversight and signals closer alignment between AML, prudential, and regulatory data sets. From a reporting perspective, 2026 is characterised by continuous regulatory movement rather than a single milestone.

Reporting as an operational capability

As supervisory expectations rise, regulatory reporting increasingly reflects institutional maturity. Data quality, automation, governance, and accountability now sit at the centre of preparedness assessments.

Experience shows that institutions with scalable data models and adaptable reporting infrastructures absorb regulatory change more effectively. They limit operational disruption, respond faster to supervisory demands, and maintain consistency across reporting cycles.

In 2026, the defining question for financial institutions is not which regulation will arrive next. It is whether their reporting capability is resilient enough to evolve continuously. Those that treat regulatory reporting as operational infrastructure rather than a reactive compliance task are better positioned to operate with confidence in an increasingly complex supervisory environment.